Introduction: The Dawn of a New Financial Empowerment Era

The socio-economic landscape of West Bengal is undergoing a massive transformation with the rollout of the flagship Annapurna Yojana. Introduced as a core pillar of the state’s updated governance and welfare model, this ambitious direct benefit transfer (DBT) scheme aims to provide unprecedented financial stability to women across the state. By placing financial resources directly into the hands of the female heads of households, the scheme is designed to foster independent decision-making, alleviate rural poverty, and drive grassroots consumer spending.

For years, West Bengal has been a testing ground for massive social security cash transfers. However, the scale, reach, and monetary volume promised under the new Annapurna Yojana mark a significant departure from previous initiatives. In an era where economic resilience at the household level dictates a state’s overall progress, this program stands out as a critical intervention. This comprehensive guide will break down every aspect of the scheme, evaluating its structure, target demographics, financial implications, and operational roadmap.

The Core Objectives of the Scheme

At its heart, the Annapurna Yojana is built upon the principle of gender-targeted financial inclusion. The primary objective is to guarantee a predictable, monthly baseline income for women who manage households, particularly those from economically marginalized backgrounds. By ensuring that financial aid is not a one-time grant but a sustained monthly inflow, the Annapurna Yojana seeks to insulate vulnerable families from sudden inflationary shocks and seasonal income drops.

Furthermore, the Annapurna Yojana looks at welfare through the lens of dignity rather than mere charity. When a woman receives direct state backing, her status within the family unit and the local community shifts positively. The West Bengal government envisions the Annapurna Yojana as a tool to bridge the gender wealth gap, allowing women to fund emergency medical needs, children’s auxiliary education, or small-scale entrepreneurial endeavors without relying on informal, high-interest local moneylenders.

Financial Architecture: What Does the Scheme Offer?

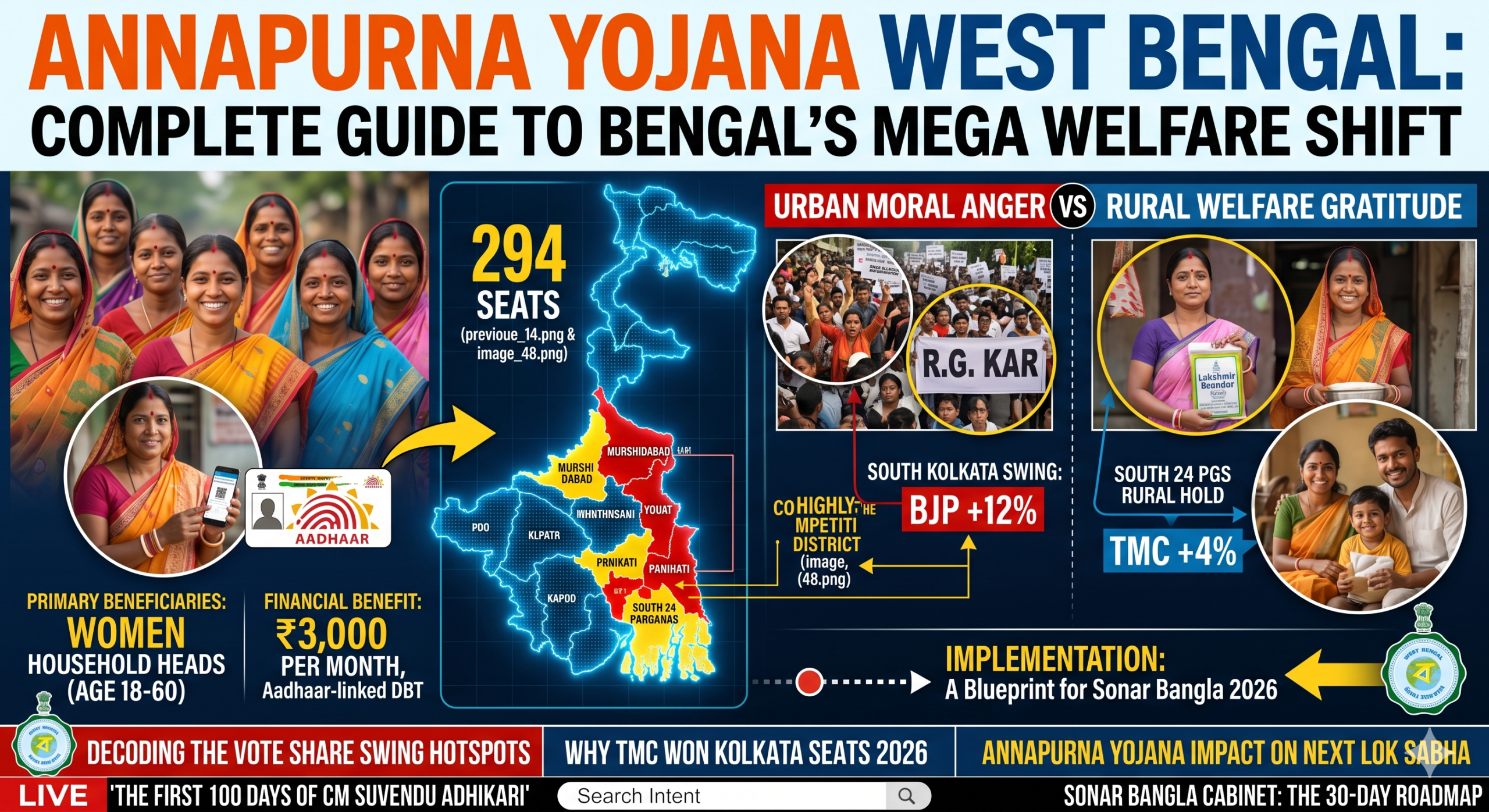

The financial commitment behind the Annapurna Yojana is staggering, making it one of the largest state-level DBT programs in contemporary India. Under the rules of the Annapurna Yojana, eligible women across the state receive a direct monthly cash transfer of ₹3,000. This uniform amount represents a significant upward revision in the state’s traditional welfare baseline, ensuring that the purchasing power of rural and urban underprivileged households is substantially enhanced.

The transfer mechanism of the Annapurna Yojana is entirely digital, leaving no room for middlemen, administrative leakages, or local institutional corruption. The funds are routed directly from the state treasury to the Aadhaar-linked bank accounts of the beneficiaries. This automated pipeline ensures that on a designated date every month, the financial benefits of the Annapurna Yojana reach the intended recipient seamlessly, providing a reliable fiscal rhythm to millions of households.

Eligibility Criteria: Who Can Benefit from the Scheme?

To ensure that the massive financial resources allocated for the Annapurna Yojana are utilized effectively, the state government has laid down clear, transparent eligibility benchmarks. The scheme is fundamentally designed for permanent residents of West Bengal. Any woman applying for the Annapurna Yojana must be a legal resident of the state and fall within the designated age bracket, which typically targets adult women managing households, generally between 18 and 60 years of age.

Social inclusivity is a major highlight of the Annapurna Yojana‘s deployment strategy. The program deliberately lowers barriers for women belonging to Scheduled Castes (SC), Scheduled Tribes (ST), and other historically disadvantaged communities. While the Annapurna Yojana aims for universal coverage among underprivileged households, families with permanent government employees or high-bracket income tax payers are excluded to ensure that the fiscal benefits strictly prioritize those who need a social safety net the most.

How to Apply: A Step-by-Step Operational Breakdown

Recognizing that a complex application process can inadvertently exclude the most vulnerable segments of society, the implementation team behind the Annapurna Yojana has simplified the registration pipeline. The government has introduced a hybrid application model, allowing citizens to apply for the Annapurna Yojana through both accessible digital portals and localized physical outreach camps. This double-pronged approach ensures that rural women with limited digital literacy are not left behind.

For physical applications, dedicated government mobilization camps—organized at the Gram Panchayat and municipal ward levels—serve as primary data collection hubs for the Annapurna Yojana. Applicants need to submit basic verifying documents, including their Aadhaar card, ration card, residential proof, caste certificate (if applicable), and crucially, active bank account details. Once the documents are verified by local block development officials, the applicant is registered into the centralized Annapurna Yojana database, activating the monthly payment cycle.

The Socio-Economic Impact on Rural Bengal

The immediate ramifications of the Annapurna Yojana are most visible across rural West Bengal, where agrarian economies often face volatile market cycles. By injecting hundreds of crores of rupees directly into village micro-economies every single month, the Annapurna Yojana acts as a localized economic multiplier. The consistent cash influx stimulates demand for daily essentials, locally produced agricultural goods, and small retail commodities, keeping rural marketplaces vibrant.

From a sociological perspective, the scheme fundamentally alters intra-household financial dynamics. In many traditional setups, women lack direct access to cash, making them dependent on male family members for minor daily expenditures. With the arrival of the scheme funds, these women gain an autonomous wallet. This financial agency directly influences nutritional choices for young children, allows for immediate healthcare spending, and builds a sustainable psychological cushion against sudden economic duress.

Empowering the Urban Underprivileged Communities

While the rural impact of the program is vast, the scheme is equally vital for the urban poor living in municipal slums and industrial fringes. Urban poverty presents unique challenges, primarily driven by high costs of living, unregulated rental markets, and erratic informal sector employment. For a domestic worker, a daily wage laborer, or a street vendor in Kolkata or Asansol, the guaranteed support of the scheme provides an invaluable baseline security mechanism.

In urban setups, the ₹3,000 monthly cash transfer from the Annapurna Yojana often goes directly toward fixed overheads, such as electricity bills, clean drinking water access, or public transport costs for working women. By easing these rigid monthly pressures, the Annapurna Yojana enables urban poor families to allocate their irregular informal wages toward better livelihood opportunities, technical skill development for youth, and escaping the persistent cycle of urban poverty.

Budgetary Allocation and Fiscal Sustainability Challenges

Executing a welfare program of the magnitude of the Annapurna Yojana requires an extraordinary commitment from the state exchequer. Skeptics and financial analysts frequently raise questions regarding the long-term fiscal sustainability of such a massive recurring cash transfer. Allocating thousands of crores annually for the Annapurna Yojana means that the West Bengal finance department must carefully balance its developmental capital expenditure with revenue expenditure.

To ensure that the Annapurna Yojana remains fiscally sustainable without driving the state into a severe debt trap, the government is focusing on strict data auditing. By leveraging advanced data analytics and cross-referencing beneficiary lists with central tax databases, the state is systematically eliminating duplicate, fraudulent, or ineligible profiles from the Annapurna Yojana roster. This rigorous cleanup ensures that every rupee spent optimizes social welfare efficiency while safeguarding the state’s broader macroeconomic health.

The Role of Technology in the Annapurna Yojana Ecosystem

Technology acts as the invisible backbone ensuring the success and transparency of the Annapurna Yojana. The entire lifecycle of a beneficiary’s interaction with the scheme—from initial data entry and document verification to the ultimate direct treasury disbursement—is tracked via a customized, secure software architecture. This digital governance model eliminates bureaucratic delays that historically plagued old-school welfare distribution systems.

Furthermore, the integration of the Public Financial Management System (PFMS) within the Annapurna Yojana structure allows for real-time tracking of failed transactions. If a bank account bounce occurs due to an incorrect IFSC code or an unlinked Aadhaar, the system immediately flags the issue for local administrative correction. This emphasis on tech-driven precision protects poor beneficiaries from losing out on their monthly Annapurna Yojana allowances due to minor technical glitches.

Comparing Annapurna Yojana with Historical Precedents

To truly appreciate the systemic scale of the Annapurna Yojana, it is helpful to contrast it with previous gender-focused cash transfer programs in West Bengal, such as the legacy Lakshmir Bhandar scheme. While older iterations laid the vital foundational groundwork for direct cash transfers to women, they often featured lower financial outlays and faced periodic bureaucratic bottlenecks. The Annapurna Yojana represents an evolution, doubling the financial quantum and heavily modernizing the backend delivery infrastructure.

By elevating the monthly transfer to a uniform ₹3,000, the Annapurna Yojana acknowledges the reality of modern inflationary pressures on lower-income families. Furthermore, unlike older schemes that occasionally featured complex tier systems based strictly on social stratification, the Annapurna Yojana adopts a more universally aggressive posture toward alleviating economic distress, making it a much more comprehensive safety net for the modern socio-economic landscape.

Synergy with Central Government Schemes

The West Bengal government is actively working to ensure that the Annapurna Yojana does not operate in an administrative silo. Instead, efforts are being made to establish strategic synergies between this state initiative and various Central Government social security networks. For instance, when a woman combines her Annapurna Yojana monthly allowance with benefits from central housing, sanitation, or subsidized cooking gas programs, the cumulative upward mobility effect on the household is profoundly accelerated.

This inter-governmental synergy turns the Annapurna Yojana into an essential component of a multi-layered financial defense mechanism for poor families. While central schemes often focus on asset creation—like building concrete houses or providing tap water connections—the Annapurna Yojana provides the liquid cash necessary for daily survival and operational maintenance, perfectly complementing structural development with immediate, liquid livelihood support.

Addressing Challenges: Eliminating Middlemen and Field Hurdles

No mass welfare rollout is entirely free from ground-level implementation challenges, and the Annapurna Yojana is no exception. In the initial phases, field officers reported minor hurdles, including erratic internet connectivity in remote deltaic regions of the Sundarbans, biometric mismatches during Aadhaar verification, and localized misinformation spread by unauthorized political intermediaries trying to exploit illiterate applicants.

In response to these localized challenges, the state administration took a proactive, zero-tolerance stance to preserve the integrity of the Annapurna Yojana. Special grievance redressal cells were established in every district headquarters, operating independently of local political interference. Field verification officers were equipped with offline data collection applications, ensuring that geographical remoteness or temporary network blackouts could not block a deserving woman from registering for her legitimate Annapurna Yojana benefits.

The Impact on Women’s Health and Domestic Nutrition

An often overlooked but vital outcome of sustained cash transfer initiatives like the Annapurna Yojana is their direct correlation with improved public health metrics. In lower-income households, when finances run tight, nutritional sacrifices are disproportionately borne by women and young girls. With the guaranteed monthly cash inflow from the Annapurna Yojana, beneficiary families can afford a more diverse, protein-rich diet, including regular access to milk, eggs, and fresh vegetables.

Additionally, the Annapurna Yojana funds give women the financial power to seek timely medical intervention for chronic illnesses rather than ignoring symptoms due to lack of immediate cash. Whether it is paying for diagnostic tests at local clinics or buying prescribed monthly medications, the liquidity provided by the Annapurna Yojana directly reduces out-of-pocket health expenditure emergencies, which are historically the leading cause of vulnerable families slipping back into deep poverty.

Boosting Micro-Entrepreneurship and Self-Help Groups (SHGs)

An exciting secondary wave of transformation triggered by the Annapurna Yojana is the rise of rural micro-entrepreneurship. Across various districts, women are choosing to pool a portion of their monthly Annapurna Yojana disbursements within local Self-Help Groups (SHGs). This collective pooling creates an informal community venture capital fund, allowing members to take out small business loans to purchase sewing machines, livestock, or artisanal raw materials.

By transforming a pure consumption welfare dole into productive economic capital, these women are maximizing the structural potential of the Annapurna Yojana. The state government is observing this trend closely and planning auxiliary training programs to help ambitious Annapurna Yojana recipients scale up their home-grown micro-enterprises, thereby converting a basic state welfare dependency into a sustainable model of long-term financial self-reliance.

Public Perception, Media Narrative, and Grassroots Feedback

The public discourse surrounding the Annapurna Yojana across West Bengal is intensely vibrant. On the ground, the feedback from beneficiaries is overwhelmingly positive, with millions of women referring to the monthly transfer as an indispensable pillar of their household budget. For these citizens, the predictability of the Annapurna Yojana payout offers peace of mind that cannot be quantified by macroeconomic data points alone.

In the regional media, the narrative balances praise for the scheme’s flawless execution with analytical debates regarding the state’s fiscal layout. Editorials frequently emphasize that while the immediate humanitarian relief provided by the Annapurna Yojana is undeniable, its ultimate legacy will depend on how efficiently the state pairs this liquid cash injection with industrial job creation and structural economic modernization to ensure holistic, multi-dimensional progress for the generation to come.

Conclusion: The Lasting Legacy of the Annapurna Yojana

The Annapurna Yojana of the West Bengal government has firmly established itself as a landmark experiment in large-scale social security planning. By successfully delivering a robust, tech-enabled, monthly financial cushion of ₹3,000 directly to millions of women, the program has set a high standard for how sub-national governments can address structural poverty and gender-based financial marginalization in the modern era.

As the program navigates its future implementation cycles, its success will offer valuable lessons to policymakers across developing economies. Ultimately, the Annapurna Yojana proves that targeted welfare, when executed with absolute transparency and digital precision, does more than just distribute funds—it builds a foundation of long-term security, dignity, and economic resilience for the entire state.

Key Takeaways

| Feature | Details |

| Name of the Scheme | Annapurna Yojana, West Bengal |

| Primary Beneficiaries | Adult Women (Household Heads, age 18-60) |

| Financial Benefit | ₹3,000 per month transferred directly |

| Transfer Mode | Aadhaar-linked Direct Benefit Transfer (DBT) |

| Core Intent | Financial inclusion, poverty reduction, female agency |

| Application Channels | Localized Outreach Camps & Centralized Online Portals |

To read about the structural administrative framework that handles this scheme’s rollout, see our deep-dive analysis on The First 100 Days of CM Suvendu Adhikari: A Blueprint for West Bengal’s New Dawn.

For an examination of the legislative and constitutional powers guiding state treasury expenditures, explore our detailed guide on West Bengal Governor Raj Bhavan Powers Explained.

To review certified state data tracking beneficiary registration metrics, visit the official Election Commission of India (ECI) analytics hub.

To inspect the state’s budget allocation parameters for flagship direct cash transfer schemes, consult the current policy guidelines at the West Bengal Finance Department.